Oil is Not Just Fuel. It’s Everything.

This morning, before you reached your office, you’d already touched crude oil more than a dozen times. The toothbrush in your hand is plastic, made from crude. Same for the toothpaste tube. The gym t-shirt you put on is mostly polyester, a crude derivative. The road outside, mostly bitumen, another crude product. The tyre on your bike or car is made from synthetic rubber, which also comes from crude.

The headlines talk about petrol prices. The real story runs much deeper.

Background First

In late February, the US and Israel launched strikes on Iran’s nuclear facilities. Iran retaliated, and almost immediately, attention turned to the Strait of Hormuz, a 33-kilometre stretch of water through which roughly one-fifth of the world’s oil supply passes.

Iran moved to restrict shipping through it, and oil prices surged sharply, touching nearly $100 a barrel. The situation remains heated, but the fact remains: when a single chokepoint comes under threat, the entire global oil supply chain feels it.

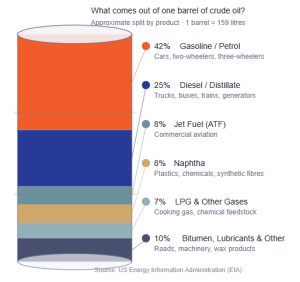

What Comes Out of a Barrel

A barrel of crude doesn’t just become petrol. About 42% becomes petrol (gasoline). Another 25% becomes diesel. The remaining third is where things get interesting.

Jet fuel for aviation. LPG for your kitchen cylinder (gas pipeline is CNG which is Natural Gas). Bitumen for roads. Lubricants for every machine with moving parts. And most importantly, naphtha, the piece many haven’t heard of.

Refineries convert naphtha into ethylene and propylene which are the building blocks of almost every plastic, synthetic rubber, and industrial chemical made today. That’s what connects a barrel of crude oil to your floor tiles, the paint on your wall, the polyester in your shirt, and the packaging around almost everything you buy.

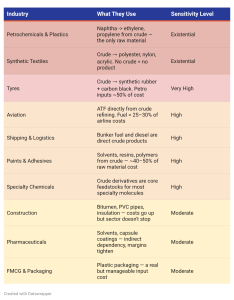

Which Industries Depend on It, and How Much

When Stocks Get Punished More Than They Should

When crude spikes, markets react quickly. Sometimes faster than the actual business impact justifies. Stocks across paints, tyres, tiles, fertilizers, and textiles have sold off hard. Some of that pain is real. But history shows that markets tend to price in the worst case, not the most likely one.

For long-term investors, this creates an interesting pattern. When a company with genuine pricing power, a leading paint brand, a top ceramics player, sees its stock fall 15–25% because crude spiked, it is worth asking one question: Is this a business problem, or a cost problem?

Business problems are structural and take years to fix. Cost problems are cyclical.

Companies with strong brands, market leadership, and the ability to pass on costs over time have historically recovered their margins when input prices normalized. Companies in commoditized segments without pricing power tend not to.

Understanding which bucket a company falls into will help you invest in the right company at the right time.

If you enjoyed this newsletter, feel free to share it with your friends and family!

Till the next time,

Vijay

CEO – InCred Money