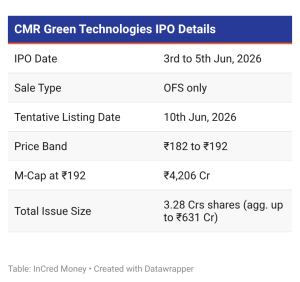

Brief IPO Highlight

The Big Picture

India’s aluminium industry runs on two tracks.

Primary aluminium is made by smelting bauxite ore. Hindalco and Vedanta run large primary smelting operations. But it’s expensive to produce and carbon heavy.

The second is recycled aluminium. Recyclers extract aluminium from scrap and sell it to manufacturers. This process emits upto 97% less emissions.

CMR Green Technologies Limited is one of the market leading non-ferrous metal recycler primarily dealing in aluminium.

Going live on June 3, 2026, the IPO closes on June 5th. The offering is an Offer for Sale only, of 3.29 Cr shares, worth Rs 631 Cr, mostly to raise liquidity for the promoters.

The Business Model

CMR operates mainly across two verticals:

- Aluminium and zinc alloys: Sold primarily to automotive OEMs and Tier 1 companies as liquid aluminium alloy (37% of volume alone as on 9MFY26), aluminium ingots (35% volume), and zinc alloys (1.3% volume).

- Segregation and recycling of other metals such as stainless steel, copper, brass, lead, and magnesium. After sorting the aluminium, these metals are sold as segregated, furnace-ready scrap to manufacturers like Jindal Stainless and Aurubis.

CMR operates 13 recycling facilities with a combined installed capacity of 6 lakh MTPA as of 9MFY2026.

Among domestic peers, CMR is the only player with multiple Japanese joint venture partners like Nikkei MC, Toyota, among others. This gives it access to proprietary temperature-control and quality-monitoring technology calibrated to Japanese OEM specifications.

The National Opportunity for Aluminium

- The recycled aluminium market in India is expected to reach $9 billion by FY30 up from ~$5 billion in FY25. OEM Scope 3 targets make the shift to recycled metals non-optional. This makes it a very high growth and lucrative market.

- CMR holds ~45% market share by volume in India’s automotive cast alloy segment in FY25. Its installed capacity is approximately 4x the nearest domestic competitor.

- Liquid aluminium supply requires plants within ~25 km of the customer. This limits liquid supply in India to a small set of technically capable, well-capitalised players, of which, CMR is the largest by far.

Operational KPIs

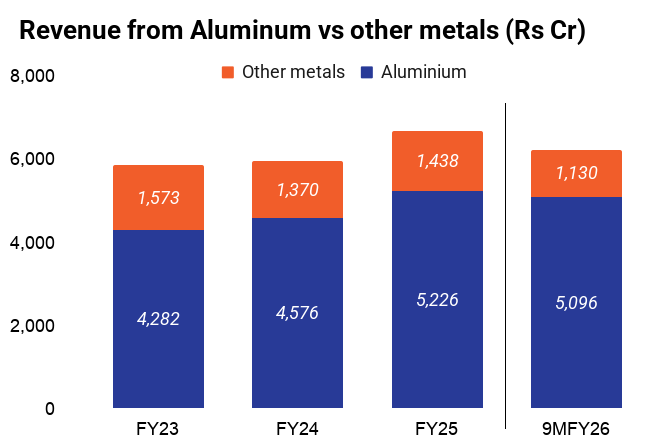

- Aluminium alloy revenue rose ~20% from Rs 4,282 Cr in FY23 to Rs 5,226 Cr through FY25, while other metals revenue fell ~8% from Rs 1,573 Cr to Rs 1,438 Cr.

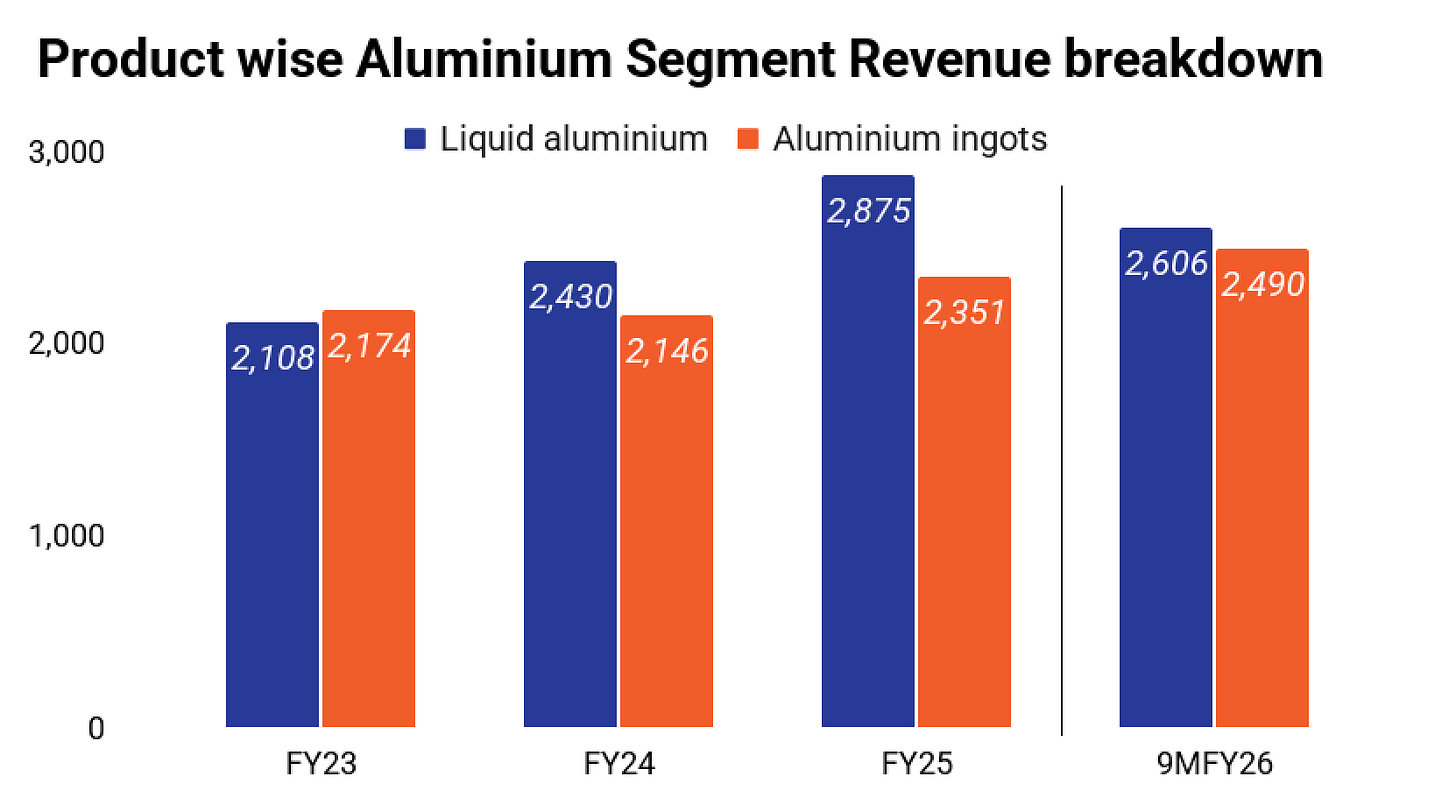

- Revenue Share of liquid aluminium has been increasing. Liquid aluminium’s revenue share rose from 49% in FY23 to 55% in FY25. It should be noted that if any clients relocate their factories, it would be costly for CMR to relocate their units to be close to the new locations.

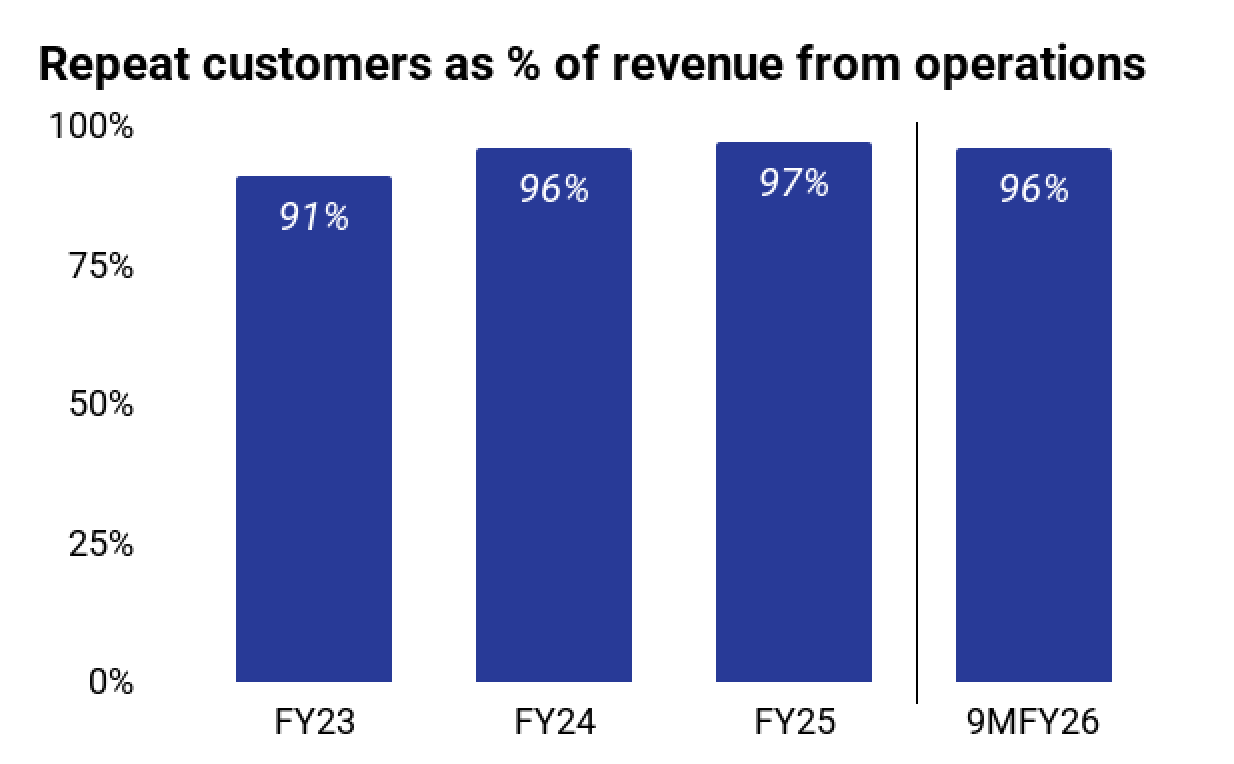

- Customer retention. Repeat customers account for 97% of revenue as on FY25. Even in FY23, this was at 91%. In this line of business, it makes sense to have a long term relationship between parties as the cost of switching would be very high, and also CMR is a market leader in recycled metals, giving clients more incentive to not switch.

Peer Comparison

– Gravita India earns 8.4% EBITDA margins while Century Aluminium earns 7.8%. CMR’s lower margins are because they sell overwhelmingly to automotive OEMs and Tier 1 companies, who push annual cost-downs heavily.

– Jain Resource Recycling’s revenue has grown much faster despite operating at a similar scale. JRR had 45% CAGR over FY23 to FY25 versus CMR’s 6.5%.

– CMR has also managed to maintain a low enough D/E ratio (0.58x) compared to its peers like Century Aluminium as well as Baheti Recycling, both with a 2.4x D/E.

Financial Analysis

- Revenue grew from Rs 5,869 Cr in FY23 to Rs 6,666 Cr in FY25 growing at a CAGR of 6.5%. While FY23 to FY24 was essentially flat. The growth in FY25 and 9MFY26 reflect capacity additions due new plant contributions.

- PAT Margins increased from 1.79% in FY23 to 2.58% in 9MFY26. After stripping the FY24 goodwill write-off, the PAT trend is upward but not steep.

- Finance costs reached Rs 67 Cr in 9MFY26 against an EBITDA of Rs 324 Cr. Interest coverage ratio is ~4.8x slightly down from 5x in FY23.

Risk Analysis

- 49.8% of imports come from the US alone. A disruption like tariff changes on scrap exports, port disruptions, or dollar-rupee volatility compresses margins. The company does partially hedge forex risk via forward contracts.

- Customer Concentration Risk: CMR relies heavily on a limited client base, with its top five customers contributing 32.5% of consolidated revenue as of December 2025. This lack of diversification leaves the company vulnerable to significant financial impact if a key client reduces orders or switches to a competitor.

Glance at Valuation

Conclusion

CMR is the right business in the right industry at an important moment in India’s story. The aluminium recycling sector in India is large, growing, and increasingly mandated by OEM emissions targets. CMR occupies the dominant position and has partnerships with Toyota and Nikkei.

The real concern is that debt has nearly tripled in three years and all bets are on two new plants in Tirupati, and Odisha, both where CMR has limited track record.