IPO Summary

The Big Picture

Specialized nutrition products are rapidly gaining momentum in India. Valued at ₹1.53 lakh crore in 2025, the market is projected to reach ₹2.81 lakh crore by 2030.

This robust growth is primarily driven by:

- Rising living standards: A structural shift toward proactive health and wellness lifestyles.

- Heightened clinical awareness: Greater consumer and medical recognition of targeted clinical nutrition.

- Surging chronic health needs: A growing prevalence of micronutrient deficiencies, vitamin gaps, and lifestyle diseases.

Another point to note: over 80% of India’s population still suffers from micronutrient and vitamin deficiencies, diabetes and chronic kidney diseases. Each of these conditions becomes a indirect demand driver for specialised nutrition products.

On the supply side, India imports ~ $980 Mn and exports ~$70 Mn of nutraceutical goods like vitamins and mineral supplements. Also, China supplies 25% of India’s raw material imports for this sector.

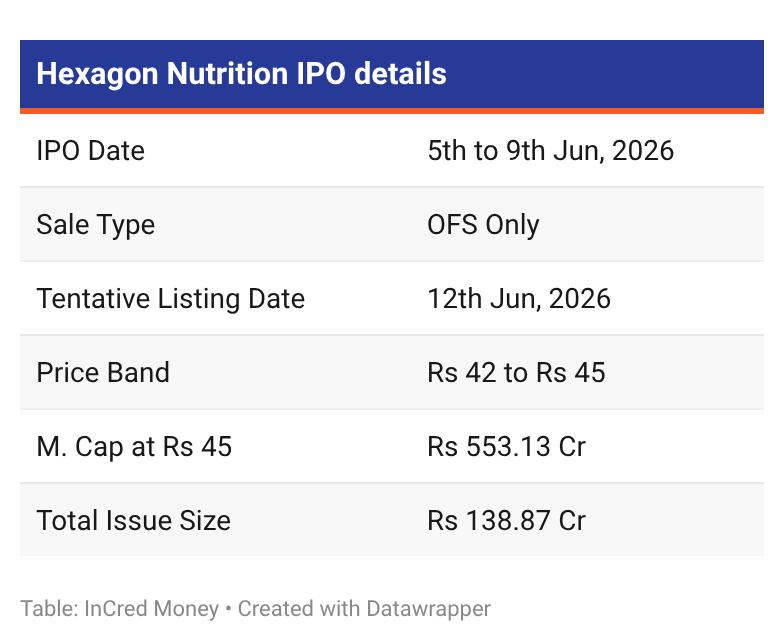

Hexagon Nutrition Limited is going live today with a pure Offer for Sale of up to 3.09 Cr shares worth Rs 138.87 Cr, with the offer window opening Friday, June 5, 2026 and closing on June 9.

The Business Model

Hexagon Nutrition, incorporated in 1993, is India’s only Integrated Nutrition player. It operates across three revenue segments:

• Premix Formulations (B2B2C): This was ~51% of 9MFY26 revenue. It includes custom vitamin and mineral premixes sold to global FMCG companies. Hexagon is one of India’s largest premix players.

• Branded Clinical Nutrition (B2C): This was ~30% of 9MFY26 revenue. This is Hexagon’s own brands, namely Pentasure (ICU and post-surgical recovery), Obesigo (bariatric nutrition), and Pediagold (paediatric nutrition). This is the highest margin and the fastest growing segment.

• Therapeutic Nutrition: Accounted for ~18.0% of 9MFY26 revenue. This is Ready-to-Use Therapeutic Foods (RUTFs) and Micronutrient Powders (MNPs) for UN agencies, NGOs, and government programmes globally.

Hexagon operates three manufacturing facilities and two in-house R&D centres, and has a presence across 70+ countries.

The National Problem of Malnutrition

• Micronutrient deficiency: Iron deficiency affects 57% of women and 67% of children. Vitamin D deficiency affects over half of the adult population. Zinc deficiency affects half the children under five.

• FSSAI fortification mandates: The Food Safety and Standards Authority of India (FSSAI) has mandated fortification of mass-consumption staples (rice, milk, etc). Every tonne of fortified food requires a vitamin and mineral premix blend. Hexagon is one of India’s largest premix manufacturers.

• Clinical nutrition is still an emerging concept in India, and per capita clinical nutraceuticals consumption in India is lower than all developed nations. This makes it a high margin segment for players like Hexagon.

Operational KPIs

1. Revenue from exports was 64% of total revenue from operations in FY23, and fell to 61% as of FY25. International revenue is declining slowly amidst global trade pressures.

2. Branded segment’s share of revenue has risen from 22% in FY23 to 28% in FY25, driven by rising adoption of PENTASURE and OBESIGO. As branded products have a much higher margin, overall blended margins are also on the rise.

3. Despite exports being 56% of total revenue, no single country exceeds 9% of foreign revenue, meaning the export base is well diversified across 80+ countries, reducing country-specific concentration risk.

Peer Comparison (FY25)

– Hexagon’s ₹325 Cr of sales comes from three revenue streams, while Nutrivita at ₹43 Cr and Compact at ₹68 Cr run narrower operations with no such diversification across segments or geographies.

– Nutrivita’s 14% EBITDA margin is slightly above Hexagon’s 12%. But Nutrivita runs a single-segment business whereas Hexagon’s margins are a mix of all three segments.

– Hexagon’s 8% PAT Margin slightly higher than its peers is because the premix manufacturing lowers the cost of goods sold in for its branded segment, and where three revenue streams spread fixed costs across a larger base.

Financial Analysis

• Revenue CAGR is a modest 8.1% from FY23 to FY25, from ₹279 Cr to ₹325 Cr. This growth rate is pretty slow and may affect future rate of expansion for Hexagon.

• PAT Margin expanded from 2% in FY23 to 8% in FY25, and with 9MFY26 already at 10%, the question is whether the slow revenue growth can increase the PAT Margin numbers any further, or will profits start to take a dip because of it.

• Finance costs are declining from Rs 4 Cr in FY24 to Rs 3 Cr in 9MFY26, as total debt fell from Rs 52 Cr in FY23 to Rs 27 Cr in FY25.

Risk Analysis

• Premix segment is exposed to the economics of monopolistic competition as there are not many competitors in that segment. Hexagon’s clients may shift to other suppliers for a better deal, and with 52% of revenue coming from this segment, this would be a huge loss in earnings.

• Raw material import dependency: India imports ~$1.8 billion of nutrition inputs annually. Vitamins, minerals, and amino acids, the primary premix inputs, are sourced largely from China (25% of imports), Germany and Switzerland. Disruptions from geopolitical tensions and rupee rate fluctuations are especially significant, and will lead to cost inflation.

Valuation

Conclusion

Hexagon Nutrition is interesting because their all-verticals capturing model is rare to see in India, and the fact that EBITDA margins doubled over the last two years is promising.

The main concerns are a slower revenue growth, and maybe the fact that it’s an OFS only issue, where owners only wish to liquidate their stake.

If you know somebody who would be interested in this IPO, please share the article!